Friday, November 20, 2009

some methods used to manipulate earnings & cash flow (specially operating cash flow)

Với các khoản phải trả (account of payable ~ A/P)

Khoản phải trả làm fát sinh dòng tiền ra (cash out flow), ko ảnh hưởng đến earning nhưng rõ ràng ảnh hưởng đến operating CF. Có 2 cách manipulation đối với A/P:

Stock option

Tiền thu đc khi bán stock option => tăng income

mặt khác:

khi mar. price tăng => option exercised càng nhiều => option demanded càng lớn

=> (hic giải thích hơi ngu. cần fải xem lại đã)

Buy back stock

Khi number of outstanding stock tăng lên => diluted EPS bị giảm nhiều so với basic EPS

=> để giảm tình trạng này: buy back stock.

Tuy nhiên, constraint của method này là:

no. of outstanding stock tăng khi option exercised

=> dùng tiền thu đc khi phát hành stock option để buy back.

nhưng stock option lại thường chỉ exercised khi mà mar. price tăng => price of stock bought back higher!

Khoản phải trả làm fát sinh dòng tiền ra (cash out flow), ko ảnh hưởng đến earning nhưng rõ ràng ảnh hưởng đến operating CF. Có 2 cách manipulation đối với A/P:

- Kéo dài thời gian thanh toán: cách này dễ hiểu rồi, khỏi phải giải thích nhiều. 1 dấu hiệu cần chú ý là số ngày phải trả (days of A/P) tăng dần.

- Tài trợ cho A/P (financing): bank hoặc 1 financial intermediary sẽ thay cty trả nợ cho chủ nợ (vì A/P fát sinh trong quá trình sản xuất kinh doanh => chủ nợ thường là nhà cung cấp, bên bán nguyên vật liệu...). Nói cách khác: cty đã đi vay để thanh toán khoản phải trả => chủ nợ mới là bank/financial intermediary => dòng tiền của khoản Nợ bị thay đổi tính chất: từ operating chuyển sang financing. Nghĩa là bây giờ khi thanh toán principal + interest thì đây sẽ là financing cash out flow, chứ ko còn là operating cash out flow nữa.

- Chứng khoán hóa các khoản phải thu: gộp các A/R lại, securitized rồi bán đi (thường là bán cho investment bank, đúng k nhở?). Mìh ko nhớ quá trình này loằng ngoằng ntn nhưng tóm lại cty sẽ đc ghi nhận 1 khoản GAIN & chưa có quy định là GAIN này để vào đâu, nên có cty sẽ ghi tăng Revenue, ghi giảm A/R...

Stock option

Tiền thu đc khi bán stock option => tăng income

mặt khác:

khi mar. price tăng => option exercised càng nhiều => option demanded càng lớn

=> (hic giải thích hơi ngu. cần fải xem lại đã)

Buy back stock

Khi number of outstanding stock tăng lên => diluted EPS bị giảm nhiều so với basic EPS

=> để giảm tình trạng này: buy back stock.

Tuy nhiên, constraint của method này là:

no. of outstanding stock tăng khi option exercised

=> dùng tiền thu đc khi phát hành stock option để buy back.

nhưng stock option lại thường chỉ exercised khi mà mar. price tăng => price of stock bought back higher!

Tuesday, November 17, 2009

Friday, November 13, 2009

website theo dõi các chỉ báo kinh tế vĩ mô

Mình thường xem ở web forexfactory này. Nó có filter hay & còn explain các chỉ số cho mìh cũng như có luôn link tới related info/analysis về chỉ số đó, sự kiện đó :). Cái mục "những chỉ số đáng chú ý của EU/Mỹ tuần tới" trên các website VN, chắc lấy từ đây mà ra :P.

À mà đợt trc mìh ko để ý. bẵng đi ít lâu ko vào, thấy nó có cả China. chả biết có china từ trc hay h mới có, mìh k nhớ

À mà đợt trc mìh ko để ý. bẵng đi ít lâu ko vào, thấy nó có cả China. chả biết có china từ trc hay h mới có, mìh k nhớ

Tuesday, November 10, 2009

Commercial Paper (CP)

Đọc hết bài về các loại fixed income, riêng CP thì bớt lại, nghĩ nó simple là thương phiếu thôi, có cái gì mà đọc. H đọc bài bác Giang viết về thị trường CP ở US mới thấy nó important ntn: cầu nối giữa financial world vs real world.

Đau đầu quá. Đi ngủ. Sáng mai sẽ đọc lại bài í, R62 nhở. ùh, & đọc CP đầu tiên. I promise! [mìh đag cố vặn đồng hồ sinh học cho nó về bthg`. haiz. hope me successful]

---

Update @ 11th Nov 09:

Đã đọc lại về CP. nhưng thấy nó ko seriously important như bác Giang đã nói: ngược lại, nó còn bảo là secondary mar. cho CP rất là little, thường investor "hold to maturity".

- Cũng có thể, đến L2, 3 mới đc học kỹ hơn ;).

- Hoặc, CP được issue từ co. đến investor luôn, tức là cái thị trường CP ở trong bài của bác G là primary mar; chứ ko fải secondary mar - như thị trường của các loại securities khác.

Dưới đây là tóm tắt 1 vài điều về CP mà mìh đã đọc.

Đau đầu quá. Đi ngủ. Sáng mai sẽ đọc lại bài í, R62 nhở. ùh, & đọc CP đầu tiên. I promise! [mìh đag cố vặn đồng hồ sinh học cho nó về bthg`. haiz. hope me successful]

---

Update @ 11th Nov 09:

Đã đọc lại về CP. nhưng thấy nó ko seriously important như bác Giang đã nói: ngược lại, nó còn bảo là secondary mar. cho CP rất là little, thường investor "hold to maturity".

- Cũng có thể, đến L2, 3 mới đc học kỹ hơn ;).

- Hoặc, CP được issue từ co. đến investor luôn, tức là cái thị trường CP ở trong bài của bác G là primary mar; chứ ko fải secondary mar - như thị trường của các loại securities khác.

Dưới đây là tóm tắt 1 vài điều về CP mà mìh đã đọc.

TIPS

Đọc được bài này của Krugman về TIPS. Chắc mìh hiểu đc 60%, mà thấy buồn cười cái giọng điệu mai mỉa của ông í. Mượn nguyên xi về đây, để dành lúc nào translate có sáng tạo :">

ko quên add luôn bài về on-the-run vs off-the-run fixed income nói chung & TIPS nói riêng từ blog bác Giang

source:http://krugman.blogs.nytimes.com/2009/11/09/tips-and-inflation-expectations/

[hahah, fải để source to oành vậy vì mìh sợ violate standard of professional, hnhư là I.C thì fải, misrepresentation :)) ]

November 9, 2009, 8:58 am

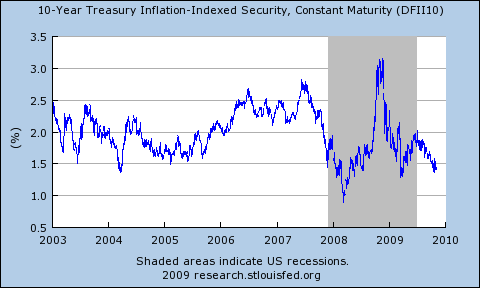

Treasury inflation-protected securities — bonds whose payouts are indexed to consumer prices — are really useful for economic analysis: they give an objective, market-based measure of expected inflation. But you have to be a bit careful about using them to interpret recent events, because the same financial disruptions that wreaked havoc with many assets also did some funny stuff to TIPS.

You can see what I mean in the chart above. The yield on TIPS shot up after Lehman fell; ordinary bond yields plunged over the same period. Was this a collapse in expected inflation? Not really, or at any rate not mostly: TIPS are less liquid than regular 10-year bonds, so in the rush for liquidity they became very underpriced for a while. Correspondingly, as markets calmed down there was a fall in TIPS yields and a rise in ordinary bond yields; this probably didn’t have much to do with changing inflation expectations.

So when you read something like this:

Oh, and this particular story did something I’ve noticed more and more in financial reporting: when reporters are assigned to write a story about how bond markets are afraid of debt/deficits/inflation, they have a strange and telling habit of telling readers a lot of scare stories about how markets are nervous, along with something about how interest rates or spreads are at their highest level in x weeks or y months — but strangely fail ever to mention what the spreads or rates actually are. Thus I’ve read scary-sounding articles about Japanese debt that somehow never mention that Japan is currently able to borrow long-term at less than 1.5%.

And in this case you’d never know from the story what the 10-year U.S. inflation rate implied by the TIPS spread is. The answer, as of Friday, was 1.98 percent. But that number sort of wouldn’t match the whole thing about bond vigilantes, I guess, so it was omitted.

ko quên add luôn bài về on-the-run vs off-the-run fixed income nói chung & TIPS nói riêng từ blog bác Giang

source:http://krugman.blogs.nytimes.com/2009/11/09/tips-and-inflation-expectations/

[hahah, fải để source to oành vậy vì mìh sợ violate standard of professional, hnhư là I.C thì fải, misrepresentation :)) ]

November 9, 2009, 8:58 am

TIPS and inflation expectations

You can see what I mean in the chart above. The yield on TIPS shot up after Lehman fell; ordinary bond yields plunged over the same period. Was this a collapse in expected inflation? Not really, or at any rate not mostly: TIPS are less liquid than regular 10-year bonds, so in the rush for liquidity they became very underpriced for a while. Correspondingly, as markets calmed down there was a fall in TIPS yields and a rise in ordinary bond yields; this probably didn’t have much to do with changing inflation expectations.

So when you read something like this:

Market inflation expectations can be calculated by comparing the difference in yields on a 10-year Treasury and a 10-year Tip. In the US, that gauge has reached the highest level in 15 months. A comparison of similar UK bonds shows expectations are at an 11-month high.you have to take it with large helpings of salt. [i like this :)) ]

This rise has led to talk of a return of “bond vigilantes”, investors who in the past have pushed up long-term bond yields on fears of inflation and forced central bankers to tighten policies.

Oh, and this particular story did something I’ve noticed more and more in financial reporting: when reporters are assigned to write a story about how bond markets are afraid of debt/deficits/inflation, they have a strange and telling habit of telling readers a lot of scare stories about how markets are nervous, along with something about how interest rates or spreads are at their highest level in x weeks or y months — but strangely fail ever to mention what the spreads or rates actually are. Thus I’ve read scary-sounding articles about Japanese debt that somehow never mention that Japan is currently able to borrow long-term at less than 1.5%.

And in this case you’d never know from the story what the 10-year U.S. inflation rate implied by the TIPS spread is. The answer, as of Friday, was 1.98 percent. But that number sort of wouldn’t match the whole thing about bond vigilantes, I guess, so it was omitted.

ý tưởng nghiên cứu US Philip curves

(bắt chước tiết mục ý tưởng nghiên cứu ktế học của bác Đỗ Quốc Anh :P)

Lúc tối đọc lại mấy cái macroeco. Nhắc lại: trong 1 business cycle (chu kỳ kinh doanh): real GDP fluctuates around potential GDP & real unemployment rate fluctuates around natural unemployment rate.

& Philip curves (đường cong Philip): mối quan hệ giữa inflation & unemployment rate:

- với short run Philip curve (SRPC): mqhệ giữa inflation & unemployment rate khi mà:

+ expected inflation = const

+ natural unemployment rate (NUR) = const

là 1 đường cong lõm, Ox: unemployment rate, Oy: inflation (rồi mìh sẽ insert hình vẽ sau) => khi real inflation > expected inflation: unemployment < NUR, vice versa (*)

- long run Philip curve: vẫn là mqhệ giữa inflation & unemployment rate, nhưng, là khi: real inflation = expected inflation

Tiện đây, có bài phân tích này về un.em. rate tháng 10/09 của US lên đến 10%. chưa đọc +_______+

---

update 10th Nov 09:

Bài này có liên quan đến real inflation vs expected inflation => FED increases interest rate. mìh đag cố từ cái logic này để suy ngược lại xem hiện h vị trí tương đối của LRPC & SRPC là ntn.

[có lẽ nào em Châu nói đúng: ôm 1 núi academic & thích academic: mìh nên đi làm giảng viên /:)]

---

update 11th Nov 09:

sửa lại tên entry cho fù hợp. US Phillip curves thì cxác hơn là US inflation :)

---

update 12th Nov 09:

expected inflation của US = 2%, theo, cái gọi là, Taylor's theory

Lúc tối đọc lại mấy cái macroeco. Nhắc lại: trong 1 business cycle (chu kỳ kinh doanh): real GDP fluctuates around potential GDP & real unemployment rate fluctuates around natural unemployment rate.

& Philip curves (đường cong Philip): mối quan hệ giữa inflation & unemployment rate:

- với short run Philip curve (SRPC): mqhệ giữa inflation & unemployment rate khi mà:

+ expected inflation = const

+ natural unemployment rate (NUR) = const

là 1 đường cong lõm, Ox: unemployment rate, Oy: inflation (rồi mìh sẽ insert hình vẽ sau) => khi real inflation > expected inflation: unemployment < NUR, vice versa (*)

- long run Philip curve: vẫn là mqhệ giữa inflation & unemployment rate, nhưng, là khi: real inflation = expected inflation

Từ cái (*) này => ý tưởng của mìh là: draw Philip curve cho US. mìh rất là tò mò với cái unemployment rate bi h thì đag ở vị trí nào trên SRPC.

- un.em. thì có rồi.

- inflation search chắc cũng có

nhưng ko biết cái expected inflation với cả NUR = ?Tiện đây, có bài phân tích này về un.em. rate tháng 10/09 của US lên đến 10%. chưa đọc +_______+

---

update 10th Nov 09:

Bài này có liên quan đến real inflation vs expected inflation => FED increases interest rate. mìh đag cố từ cái logic này để suy ngược lại xem hiện h vị trí tương đối của LRPC & SRPC là ntn.

[có lẽ nào em Châu nói đúng: ôm 1 núi academic & thích academic: mìh nên đi làm giảng viên /:)]

---

update 11th Nov 09:

sửa lại tên entry cho fù hợp. US Phillip curves thì cxác hơn là US inflation :)

---

update 12th Nov 09:

expected inflation của US = 2%, theo, cái gọi là, Taylor's theory

Mergers & acquisitions

Đọc đc 2 bài về M&A khá hay.

1 bài về Hàn Quốc cân nhắc ban hành luật cho fép thực hiện "poison pill", vì lo ngại những cty to đùng (Samsung, Posco) bị takeover. "poison pill" - liều thuốc độc, là 1 trong n~ biện fáp chống lại việc bị thâu tóm. Theo đó, nếu công ty thâu tóm (acquirer) tiến hành thương vụ đó, thì cost > benefit from M&A. Ví dụ cụ tỉ thì mìh quên rồi vì lâu ko đọc lại & chưa gặp case nào trog thực tế cả.

Bài thứ 2 nói về vụ Kraft mua Cadbury. Bthg` mìh chỉ thấy 2 bên ngấm ngầm thỏa thuận với nhau & public lúc sự đã rồi. Nhưng vì BOD của Cadbury ko accept Kraft's bid => thương vụ ko còn tính chất friendly mà chuyển thành hostile takeover & Kraft đã tiến hành chào mua công khai từ các cổ đông thường thông qua London Stock Exchange. Hahah, đúng như sách dạy, đến đoạn này thì BOD & CEO của Cadbury ra sức cho rằng giá chào mua í là quá thấp, là undervalue cty của họ; còn Kraft thì kiên quyết rằng đấy là giá hợp lý. Theo dõi 2 bên cãi nhau thú vị fết ^^.

---

update @ 10th Nov 09:

Tiện có case về M&A ở VN, thanh toán = hoán đổi CP cho vào đây. Hôm trước đọc bài báo gi gỉ gì gi kêu là M&A giữa 2 cty niêm yết chưa có tiền lệ, hem bít fải làm sao

1 bài về Hàn Quốc cân nhắc ban hành luật cho fép thực hiện "poison pill", vì lo ngại những cty to đùng (Samsung, Posco) bị takeover. "poison pill" - liều thuốc độc, là 1 trong n~ biện fáp chống lại việc bị thâu tóm. Theo đó, nếu công ty thâu tóm (acquirer) tiến hành thương vụ đó, thì cost > benefit from M&A. Ví dụ cụ tỉ thì mìh quên rồi vì lâu ko đọc lại & chưa gặp case nào trog thực tế cả.

Bài thứ 2 nói về vụ Kraft mua Cadbury. Bthg` mìh chỉ thấy 2 bên ngấm ngầm thỏa thuận với nhau & public lúc sự đã rồi. Nhưng vì BOD của Cadbury ko accept Kraft's bid => thương vụ ko còn tính chất friendly mà chuyển thành hostile takeover & Kraft đã tiến hành chào mua công khai từ các cổ đông thường thông qua London Stock Exchange. Hahah, đúng như sách dạy, đến đoạn này thì BOD & CEO của Cadbury ra sức cho rằng giá chào mua í là quá thấp, là undervalue cty của họ; còn Kraft thì kiên quyết rằng đấy là giá hợp lý. Theo dõi 2 bên cãi nhau thú vị fết ^^.

---

update @ 10th Nov 09:

Tiện có case về M&A ở VN, thanh toán = hoán đổi CP cho vào đây. Hôm trước đọc bài báo gi gỉ gì gi kêu là M&A giữa 2 cty niêm yết chưa có tiền lệ, hem bít fải làm sao

Thursday, October 29, 2009

Standards of professional conduct

Including 7 standards with 22 multiple sub-sections

B. Independence & objectivity

C. Misrepresentation

D. Misconduct

B. Market manipulation

B. Fair dealing

C. Suitability

D. Performance Presentation

E. Preservation of Confidentiality

B. Additional compensation arrangement

C. Responsibilities of supervisors

B. Communication with clients & prospective clients

C. Record retention

B. Priority of transaction

C. Referral fees

B. Reference to CFA I, the CFA Designation & the CFA Program

I. ProfessionalismA. Knowledge of the law

B. Independence & objectivity

C. Misrepresentation

D. Misconduct

II. Integrity of capital marketA. Material nonpublic information

B. Market manipulation

III. Duties to clientsA. Loyalty, prudence & care

B. Fair dealing

C. Suitability

D. Performance Presentation

E. Preservation of Confidentiality

IV. Duties to employersA. Loyality

B. Additional compensation arrangement

C. Responsibilities of supervisors

V. Investment analysis, recommendations & actionsA. Diligence & reasonable basis

B. Communication with clients & prospective clients

C. Record retention

VI. Conflicts of interestA. Disclosure of conflicts

B. Priority of transaction

C. Referral fees

VII. Responsibilities as a CFA Institute member or CFA candidateA. Conduct as member & candidate in the CFA program

B. Reference to CFA I, the CFA Designation & the CFA Program

Tuesday, October 27, 2009

Learning to love insider trading

Thấy bài này ở blog G.Mankiw. Lôi về để sau này translate. Thích kiểu của thầy Giang khi translate sang t.việt, k chỉ simple là dịch mà thầy còn làm cho nó trở nên cực cực cực kỳ dễ hiểu.

Ờ, chuyện đơn jản là: trog n~ ng` mìh biết, trong n~ tài liệu Vnese mà mìh đọc:

- có cái kiểu thuê translator dịch rồi các bác 'cốp' đứng tên => translator k fải là economist => dịch k ra gì

- có economist/ financier ... nhưg các bác:

+ hoặc là t.a prò nên tự đọc tự hiểu t.a luôn, k fải translate cho đứa nào hiểu cả!

+ hoặc là t.a qá tệ nên chỉ có vnese, vnese & vnese thôi.

Ờ, chuyện đơn jản là: trog n~ ng` mìh biết, trong n~ tài liệu Vnese mà mìh đọc:

- có cái kiểu thuê translator dịch rồi các bác 'cốp' đứng tên => translator k fải là economist => dịch k ra gì

- có economist/ financier ... nhưg các bác:

+ hoặc là t.a prò nên tự đọc tự hiểu t.a luôn, k fải translate cho đứa nào hiểu cả!

+ hoặc là t.a qá tệ nên chỉ có vnese, vnese & vnese thôi.

Monday, October 26, 2009

Understanding Financial statement (1): Income statement

* Components & formats

- Name:

- Income statement

- Statement of operations/ statement of earnings

- Profit & Loss

- Important concepts

- Revenue

- Net Income

- Subtotals:

- Gross profit = Rev - Cost of goods sold (COGS)

- Operating profit = Gross profit - all expenses related to running the business. [Operating profit <=> the firm's profits on its annual business activity before deducting taxes.

- Income after tax = Income before tax* (1-T)

- Minority interest = % income belongs to minority shareholders; subtracted from Income after tax

- Net Income = Income after tax - Minority interest

- Unbilled or accrued

- General principles

- Special case

- ... (cont.)

Sunday, October 25, 2009

Code of Ethic

- Act with integrity, competence, diligence, respect & in an ethical manner with the public, clients, prospective clients, employers, employees, colleagues in the investment profession & other participants in the global capital market.

- Place the integrity of the investment profession & the interests of clients above their own personal interests

- Use reasonable care & exercise independent professional judgment when conducting investment analysis, making investment recommendations, taking investment actions & engaging in other professional activities

- Practice & encourage others to practice in a professional & ethical manner that will reflect credit on themselves & the profession.

- Promote the integrity of, & uphold the rules governing, capital market

- Maintain & improve their professional competence & strive to maintain & improve the competence of their investment professional

PEJMAR

P - Priority: Place the integrity of the investment profession & the interests of clients above their own personal interests

E - Encouragement: Practice & encourage others to practice in a professional & ethical manner that will reflect credit on themselves & the profession.

J - Judgment: Use reasonable care & exercise independent professional judgment when conducting investment analysis, making investment recommendations, taking investment actions & engaging in other professional activities

M - Maintain: Maintain & improve their professional competence & strive to maintain & improve the competence of their investment professional

A - Action: Act with integrity, competence, diligence, respect & in an ethical manner with the public, clients, prospective clients, employers, employees, colleagues in the investment profession & other participants in the global capital market.

R - Rules: Promote the integrity of, & uphold the rules governing, capital market

Saturday, October 24, 2009

Capital asset pricing model (CAPM)

[ Beta, mìh đang muốn nói đến cái mà dùng trong Capital asset pricing model, cái mà được tính = cov(i,m)/variance m; cái mà definition là "is standardized of systematic risk". - cái này viết cho nhớ! ]

Đọc kỹ lại cái bài đấy mới thấy nó interesting hơn lúc trước mìh nghĩ. Nhất là cái phần loại đi dần2 những giả thiết của CAPM :D.

notes: khi market là efficient, thậm chí là strong efficiency, ai cũng có info. như nhau & tool như nhau. Nhưng sử dụng chúng ntn, estimate ra sao... mới là vấn đề. & 1 số investors/analyst trở thành superiors. số khác, thành inferior. 1 bên là động lực, support cho efficient mar. bên kia thì ngược lại =.=.

Đọc kỹ lại cái bài đấy mới thấy nó interesting hơn lúc trước mìh nghĩ. Nhất là cái phần loại đi dần2 những giả thiết của CAPM :D.

- Ngoài capital market line, security market line, nó còn có "characteristic line": là đồ thị hàm hồi quy E(Ri) theo beta i.

- Giả thiết nói rằng: có thể borrow @ risk-free rate, nhưng thực tế thì ko phải thế => ok, đường CML thay đổi chút chút. Cụ tỉ, nó là 1 đường gồm có

- 1 phần đoạn thẳng: khi tỷ trọng đầu tư vào danh mục thị trường (market portfolio) < 100% <=> lend @ risk-free rate => đồ thị như cũ

- 1 phần cong cong

- tiếp theo lại là đoạn thẳng: khi tỷ trọng đầu tư vào mar. port. > 100% <=> borrow @ interest rate > risk-free rate

- "zero beta": nó nói rằng ko nhất thiết fải có risk-free asset; có thể có 1 cái portfolio Z nào đó mà cov(Z, market portfolio) = zero. nói chung là câu chuyện tương tự; trừ việc market premium nhỏ đi.

- transaction cost: theo lý thuyết thì khi thấy security over/undervalued => action (sell, short sale, buy...) nhưng nhiều khi phần gain í ko bù lại đc transaction cost => nhà đầu tư chỉ 'action' đến 1 mức nào đó => securities ko nhất thiết nằm trên đường SML mà có thể nằm gần gần đấy => SML thành "band". & transaction càng nhỏ thì "band" í càng hẹp.

- heterogeneous expectations: CAPM phát triển từ Markowitz, mà 1 giả định của Markowitz là nhà đầu tư có cùng kỳ hạn đầu tư & các thứ kỳ vọng như nhau => thực tế thì kỳ hạn & kỳ vọng của NĐT là khác nhau, cũng như tax burden là khác nhau => mỗi người tự xây dựng 1 'market portfolio', tự có 1 đường CML (& SML) => aggregate: CML (SML) cũng thành "band".

DISTINGUISH BTW DIFFERENT LINES

- Efficient Frontier:

- (Markowitz's product)

- every point on this Frontier is an efficient portfolio that means having highest (expected) return while the risk (measured by standard deviation) is smallest.

- Ox: SD, Oy: E(r)

- Capital Market Line:

- every point on CML <=> a portfolio with w% invested in risk-free asset & the remain in market portfolio

- w > 0 <=> lend @ risk-free rate

- if w < 0 <=> borrow @ risk-free rate

- Ox: SD, Oy: E(r)

- Security Market Line

- Ox: beta = cov(i,m)/variance m; Oy: E(r)

- market portfolio: beta = 1

- ev'ry point on SML showed the required rate of return of a security familiar with its standardized systematic risk

- compare btw required rate of return vs expected return of a sec. => conclude whether it's overvalued or undervalued

- RR < ER <=> the sec. is above SML => undervalued

- RR > ER <=> below SML => overvalued

notes: khi market là efficient, thậm chí là strong efficiency, ai cũng có info. như nhau & tool như nhau. Nhưng sử dụng chúng ntn, estimate ra sao... mới là vấn đề. & 1 số investors/analyst trở thành superiors. số khác, thành inferior. 1 bên là động lực, support cho efficient mar. bên kia thì ngược lại =.=.

Friday, October 23, 2009

CDS, CDO & US crisis

Bác Giang đc cái là viết cực kỳ dễ hiểu :(( (hic, :(( vì xúc động & ngưỡng mộ í, chứ k fải là :(( đểu giả theo nghĩa "dễ đến mức ko thể hiểu nổi" đâu!)

Bài này tóm tắt US crisis, giải thích rõ ràng cụ tỉ CDO là j`, CDS là j`. Năm ngoái lúc học tài chính công, làm research về vđề này, mà qả thực là hồi í hiểu lơ mơ lắm í =((. Mà nói chg là mìh ngưỡng mộ US financial mar cực kỳ, từ hồi học Derivatives í (hồi đó chú HH cũng giải thích CDO với CDS dưg rồi mìh cũng quên luôn!), thấy bọn nó thông minh kinh khủng. Trời, k biết fải giỏi toán (nói chung), giỏi kinh tế lượng, mô hình toán... ntn mới nghĩ ra đc lắm thứ nthế nhở!

Thôi từ h mìh gọi bác Giang là thầy. Bác có nhận hay ko thì kệ bác, mìh gọi cứ gọi :-"

---

update 10th Nov 09: Hic cái này hay chết ruồi. Ko cho vày đây thì fí nửa đời!

part 1

part 2

Bài này tóm tắt US crisis, giải thích rõ ràng cụ tỉ CDO là j`, CDS là j`. Năm ngoái lúc học tài chính công, làm research về vđề này, mà qả thực là hồi í hiểu lơ mơ lắm í =((. Mà nói chg là mìh ngưỡng mộ US financial mar cực kỳ, từ hồi học Derivatives í (hồi đó chú HH cũng giải thích CDO với CDS dưg rồi mìh cũng quên luôn!), thấy bọn nó thông minh kinh khủng. Trời, k biết fải giỏi toán (nói chung), giỏi kinh tế lượng, mô hình toán... ntn mới nghĩ ra đc lắm thứ nthế nhở!

Thôi từ h mìh gọi bác Giang là thầy. Bác có nhận hay ko thì kệ bác, mìh gọi cứ gọi :-"

---

update 10th Nov 09: Hic cái này hay chết ruồi. Ko cho vày đây thì fí nửa đời!

part 1

part 2

"write-down", "mark to market", "valuation allowance", "LIFO liquidation layer", "LIFO reserve"

[Đặt cục gạch, đọc xong nốt rồi sẽ viết. Cái này thú vị àh, hôm trước đọc blog bác Giang mà lúc í chưa hiểu áh.]

[Update 27th Oct 09:

1. Bổ sung thêm bài viết này có liên quan đến mark-to-market. Bài này nói về quy định của kế toán Mỹ đối với asset ở công ty tài chính; loại nào thì mark-to-market (đag thắc mắc "cty tài chính" là cái gì. Commercial bank, investment bank, hay cty cho thuê tài chính... hay cái gi gỉ gì gi???)

2. Tóm tắt cho bài Inventories: so sánh giữa US GAAP & IFRS: 2 điểm khác nhau lớn nhất.

1 là US cho fép dùng LIFO nhưng IFRS thì ko

2 là: khi đã write down, IFRS cho fép 'recover' nhưng US thì ko]

[Update 27th Oct 09:

1. Bổ sung thêm bài viết này có liên quan đến mark-to-market. Bài này nói về quy định của kế toán Mỹ đối với asset ở công ty tài chính; loại nào thì mark-to-market (đag thắc mắc "cty tài chính" là cái gì. Commercial bank, investment bank, hay cty cho thuê tài chính... hay cái gi gỉ gì gi???)

2. Tóm tắt cho bài Inventories: so sánh giữa US GAAP & IFRS: 2 điểm khác nhau lớn nhất.

1 là US cho fép dùng LIFO nhưng IFRS thì ko

2 là: khi đã write down, IFRS cho fép 'recover' nhưng US thì ko]

Bài này về Inventories - hàng tồn kho.

- Hàng tồn kho có thể ở 3 dạng: nguyên vật liệu (thô), sản phẩm dở dang & thành phẩm. IFRS & US GAAP quy định rằng nếu ko được tách bạch rõ ràng ở Balance sheet thì nó fải đc trình bày ở footnote của financial statements.

- Các khoản mục được tính vào 'capitalized inventory cost', tức là giá trị của hàng tồn kho:

- purchase cost - chi phí mua hàng

- conversion

- portion of fixed overhead cost (ko biết dịch là gì), with portion = real productivity/capacity level of production (*)

- cost related to bringing the invent. to present position & condition

- Các khoản mục ko đc tính vào giá trị hàng tồn kho mà cho vào Expense trong kỳ:

- abnormal costs: material wasted

- abnormal waste for labor cost & overhead cost

- storage cost

- all administrative overhead & selling cost

- the remain of (*): eg. 90% overhead cost belongs to capitalized inventory cost =>10% belongs to expense.

- Value of invt. recorded = min (historical cost, Net realized value):

- Historical cost <=> carrying cost <=> cost carried on Balance sheet

- NRV = Estimated selling price in ordinary course of business - Estimated costs necessary to make the sale

- "mark-to-market": the process used to adjust asset's value to reflect current "fair" value (always realized by market price).

- WRITE DOWN:

- If "fair value" of Invt decreases => record "write-down": decrease Invt on BS while increase Expense on IS

- the amount write-down <=> valuation allowance.

- When the fair value recovers => under IFRS: reversal write-down. but under US GAAP: NO accept reversal (after write-down, it could only be written down more!)

- Reversal is limited: "fair value" <= historical cost. However, firms produce agricultural, forest, mineral products & dealer firm have NO limitation.

- Invt. Accounting method: FIFO, WAC, specific (under IFRS) & US.GAAP has 1 more: LIFO. For co. using LIFO method:

- Must to compute LIFO reserve:

- = FIFO Invt. value - LIFO Invt value.

- Meaning: use in comparison btw co. using LIFO & FIFO, or in order to value the co. as if using FIFO method

- Converse COGS: COGS (under FIFO) = COGS (under LIFO) - (LIFO reserve this term - LIFO reserve last term)

- LIFO liquidation: happens in rising-price period, when unit of Ending Invt < Beginning Invt: some of Profit earned by using old inventories in production. It's called "phantom profit".

Comprehensive Income

Hôm trước đọc bài này nghĩ là "bọn VN sao lại đi ngược IAS/ IFRS thế, cái đấy fải cho vào comprehensive income chứ nhỉ". Mà giờ thì thấy mình sai bét be rồi.

Theo US GAAP:

Comprehensive income (ko biết dịch ra t.việt tn, quên mất thuật ngữ t.việt of nó rồi, hic) là n~ khoản làm thay đổi Equity, gồm: Net Income + Other comprehensive income (OCI)

Net Income lấy từ Income statement rồi; còn OCI là n~ khoản ko thuộc Income statement. Cụ tỉ gồm:

(IFRS quy định tương tự nhưng ko gọi đấy là OCI mà thôi.)

Tóm lại: đến giờ vẫn ko biết exactly chênh lệch tỷ giá (giả sử, khi mìh bán hàng ra nước ngoài) hạch toán ntn, nhưng mà chắc chắn là nó ko fải là cái thứ đc tính vào OCI.

Theo US GAAP:

Comprehensive income (ko biết dịch ra t.việt tn, quên mất thuật ngữ t.việt of nó rồi, hic) là n~ khoản làm thay đổi Equity, gồm: Net Income + Other comprehensive income (OCI)

Net Income lấy từ Income statement rồi; còn OCI là n~ khoản ko thuộc Income statement. Cụ tỉ gồm:

- Foreign currency translation: Chênh lệch tỷ giá khi lập Báo cáo tài chính hợp nhất (financial statement consolidation), mà cty con (subsidiaries) thuộc qgia khác => fải chuyển đổi về chung 1 đvị tiền tệ.

- Unrealized gain/loss of available-for-sale securities: Đối với trading securities (chứng khoán giao dịch) thì gain/loss được phản ánh ở Income statement nhưng với available-for-sale securities (chứng khoán sẵn sàng để bán) thì unrealized gain/loss ko qua IS mà chuyển thẳng vào OCI. (notes: khác nhau giữa 2 loại chứng khoán này là: trading sec. là n~ CK để giao dịch thường xuyên (actively traded). Ngoài 2 loại này còn 1 loại investment securities nữa đấy là "hold to maturity securities" => vì được giữ đến khi đáo hạn => ko cần quan tâm đến unrealized gain/loss khi market price thay đổi)

- Gain/loss of derivatives which qualify as NET investment hedges or cash flow hedges

- Minimum pension liability adjustments from underfunded defined-benefit plans

(IFRS quy định tương tự nhưng ko gọi đấy là OCI mà thôi.)

Tóm lại: đến giờ vẫn ko biết exactly chênh lệch tỷ giá (giả sử, khi mìh bán hàng ra nước ngoài) hạch toán ntn, nhưng mà chắc chắn là nó ko fải là cái thứ đc tính vào OCI.

Behavioral Finance

Behavioral finance considers how various psychological traits affect the ways that individuals or groups act as investors, analysts, portfolio managers

Explain biases based on psychological characteristics:

---

~ Jan 09, I read a graduation thesis 'bout this topic. @ that time I thought that it was funny, stupid. IMO, finance market is for quantitative method, complex model, lots of math, formula, etc.

Hic. Til now I've realized its meaning (although I don't remember what mentioned in the thesis).

Vnese calls it "ếch ngồi đáy giếng".

Explain biases based on psychological characteristics:

- Prospect theory: fear losses much more than they value gains => hold on to 'losers' too long & sell 'winners' too soon. 'cos utility depends on deviations from moving reference points rather than absolute wealth.

- Overconfidence in forecasts => overestimate growth rates for growth co. & overemphasize good news while ignore negative news for the firms.

- Confirmation bias: => lead to: look for information that supports their prior opinion. eg.: consider growth co. <=> growth stock, cyclical co. vs cyclical stock, defensive co. & defensive stock...

- Noise traders: make price volatile without relevant information 'cos have no OWN opinion, tend to follow newsletter writers who in turn, also "follow the herd"

- Escalation bias => put more money into a failure (eg. "averaging down" strategy). Solution: ignore sentiment; reevaluate the stock: was there any bad new missed in the initial valuation? or if its valuation is confirmed, acquire more of this 'bargain'.

---

~ Jan 09, I read a graduation thesis 'bout this topic. @ that time I thought that it was funny, stupid. IMO, finance market is for quantitative method, complex model, lots of math, formula, etc.

Hic. Til now I've realized its meaning (although I don't remember what mentioned in the thesis).

Vnese calls it "ếch ngồi đáy giếng".

Thursday, October 22, 2009

Arbitrage constraints (related to anomalies), market efficiency

8 thêm tẹo. Hnay trong đống bài loằng ngoằng ở Cur 5 thì có nói về n~ anomalies in efficient mar => arbitrage opportunities. Tuy nhiên cũng có n~ limitation khiến arbitrage ko thực hiện đc.

Đây là 1 vdụ. Cái này thuộc về limitation of capital :) (may quá đỡ ghét cái Cur 5 đc 1 tí)

Và 2 anomalies đây nữa.

Market efficiency nữa này. Tóm tắt:

- Theory: khi có anomaly thì xảy ra arbitrage, cho tới khi profit = zero <=> all info. reflects in price => efficient mar.

- Fact: can't arbitrage => mar becomes inefficient!

Thêm 1 bằng chứng cho cái sự lucky của mìh. Biết blog bác Giang, để connect n~ thứ đag học với n~ thứ realistic. thật thích :x

(ko biết my English có kih khủng lắm ko. IMO: arbitrage constraints <=> constraints that limit arbitrage)

p/s: lại break today's plan. speed up!!!

Đây là 1 vdụ. Cái này thuộc về limitation of capital :) (may quá đỡ ghét cái Cur 5 đc 1 tí)

Và 2 anomalies đây nữa.

Market efficiency nữa này. Tóm tắt:

- Theory: khi có anomaly thì xảy ra arbitrage, cho tới khi profit = zero <=> all info. reflects in price => efficient mar.

- Fact: can't arbitrage => mar becomes inefficient!

Thêm 1 bằng chứng cho cái sự lucky của mìh. Biết blog bác Giang, để connect n~ thứ đag học với n~ thứ realistic. thật thích :x

(ko biết my English có kih khủng lắm ko. IMO: arbitrage constraints <=> constraints that limit arbitrage)

p/s: lại break today's plan. speed up!!!

Liquidity

Bài này đọc rồi. Mà quên. Post lại cho nhớ. Hình như bác Giang còn 1 bài về liquidity vs solvency. Heheeh, tìm thấy rồi.

Tóm tắt liquidity: có 2 nghĩa:

1. mar. liquidity <=> mar. depth, measured by bid-ask spread: smaller => more liquid

(update 22nd Oct 09: vừa đọc lại về liquidity. cái measured by bid-ask spread có vẻ ko hẳn đúng. nói lại theo sách nhé.

liquidity = marketability + continuity price

marketability <=> able to sell assets quickly

continuity price <=> price NOT change MUCH compared with prevail price, unless there's a new significant info.

=> these 2 things require DEPTH <=> there're numerous buyers & sellers who ready to trade @ price below or above current market price.)

2. fund liquidity <=> equity capital

& đây là liquidity vs solvency

Notes: Hôm trước làm bài bị nhầm nhá. current ratios => liquidity, còn bankruptcy liên quan tới solvency ratios.

Lại thấy bài này có liên quan, post vào đây luôn: 3 stages in crisis

Bắt đầu là liquidity, tới solvency & cuối cùng là deleverage.

p/s: làm tn nhở. dùng từ theo kiểu 'bác Giang' thì 'giới Vnese econ. blog' bây giờ có mỗi bác. hic. monopoly wá. mà blog bác nh` wá. mìh đọc mãi mãi mãi mãi vẫn chưa hết nhá!

Tóm tắt liquidity: có 2 nghĩa:

1. mar. liquidity <=> mar. depth, measured by bid-ask spread: smaller => more liquid

(update 22nd Oct 09: vừa đọc lại về liquidity. cái measured by bid-ask spread có vẻ ko hẳn đúng. nói lại theo sách nhé.

liquidity = marketability + continuity price

marketability <=> able to sell assets quickly

continuity price <=> price NOT change MUCH compared with prevail price, unless there's a new significant info.

=> these 2 things require DEPTH <=> there're numerous buyers & sellers who ready to trade @ price below or above current market price.)

2. fund liquidity <=> equity capital

& đây là liquidity vs solvency

Notes: Hôm trước làm bài bị nhầm nhá. current ratios => liquidity, còn bankruptcy liên quan tới solvency ratios.

Lại thấy bài này có liên quan, post vào đây luôn: 3 stages in crisis

Bắt đầu là liquidity, tới solvency & cuối cùng là deleverage.

p/s: làm tn nhở. dùng từ theo kiểu 'bác Giang' thì 'giới Vnese econ. blog' bây giờ có mỗi bác. hic. monopoly wá. mà blog bác nh` wá. mìh đọc mãi mãi mãi mãi vẫn chưa hết nhá!

Wednesday, October 21, 2009

Cur 5

Sắp đc 1/4 Cur 5 rồi, mà ức fát khóc nên ngồi khóc lóc 1 lúc đã.

Ôg í viết cái kiểu thật là, cứ như ko bôi ra thì người ta ko biết là ôg í jỏi. mìh tiếc là đã ko đọc Cur 5 sớm hơn để complain vào cái interview của bọn CFA. Có 110pages: mìh còn đinh ninh sung sướng lên kế hoạch là chỉ học 1 buổi thôi. Thế mà bôi ra thành 4 buổi :((.

Thôi ko khóc nữa. Gì đâu mà, thấy khó là ngồi khóc àh. 23 tuổi r chả nhẽ lại = em Hương 6 tuổi, tập viết ko viết đc số 9 thế là ngồi khóc :))

Ôg í viết cái kiểu thật là, cứ như ko bôi ra thì người ta ko biết là ôg í jỏi. mìh tiếc là đã ko đọc Cur 5 sớm hơn để complain vào cái interview của bọn CFA. Có 110pages: mìh còn đinh ninh sung sướng lên kế hoạch là chỉ học 1 buổi thôi. Thế mà bôi ra thành 4 buổi :((.

Thôi ko khóc nữa. Gì đâu mà, thấy khó là ngồi khóc àh. 23 tuổi r chả nhẽ lại = em Hương 6 tuổi, tập viết ko viết đc số 9 thế là ngồi khóc :))

Saturday, October 10, 2009

Portfolio mgnt (1): The asset allocation decision

Before talkin' or even thinkin' 'bout investment, we need to talk 'bout insurance.

Stop thinking 'bout investment till you has put smth in your insurance: for your assets (house, car, etc...), yourself, to prevent from unemployment or accident.

U could say that insurance is low return & even, waste money. However, let's do double thinking. Do u want to have a chance to use your insurance? of course, not.

Insurance is only a tool to defense risk. That means, when risks happen, you or your lover will get money:

- if the assets were broken: u could repair or buy new one with the money

- if it was an accident to u: u could spend money for hospital services & for your consume during the time.

- if u lost your job: it helps u pay for your life while looking for new job

- if, unfortunately, u died: it pays for your funeral & for your lovers, your families to maintain their life after that.

To summarize:

Stop thinking 'bout investment till you has put smth in your insurance: for your assets (house, car, etc...), yourself, to prevent from unemployment or accident.

U could say that insurance is low return & even, waste money. However, let's do double thinking. Do u want to have a chance to use your insurance? of course, not.

Insurance is only a tool to defense risk. That means, when risks happen, you or your lover will get money:

- if the assets were broken: u could repair or buy new one with the money

- if it was an accident to u: u could spend money for hospital services & for your consume during the time.

- if u lost your job: it helps u pay for your life while looking for new job

- if, unfortunately, u died: it pays for your funeral & for your lovers, your families to maintain their life after that.

To summarize:

- Insurance is for protection, not for return

- Insurance should be thought & done first, before having any investment plan

- Insurance helps us & our families, lovers to deal with unexpected problems, though typically, no one wanna have a "chance" to use the insurance money

Friday, October 9, 2009

Corp.finance 5: corporate governance

Summarize corporate governance considerations (source: cur 4, pg 156-157)

Investors & shareholders shouldTHE BOARD

- Determine whether a Company's Board has, at minimum, a majority of Independent Board Members

- Determine whether Board Members have the qualifications the Co. needs for the challenges it faces.

- Determine whether the Board & its committees have budgetary authority to hire Independent third-party consultants without having to receive approval from management

- Determine whether Board Members are elected annually, or whether the Co. has adopted an election process that staggers the terms of Board Member election

- Investigate whether the Co. engages in outside business relationship with management or Board Members, or individuals associated with them, for goods & services on behalf of the Co.

- Determine whether the Board has established a committee of Independent Board Members, including those with recent & relevant experience of finance & accounting, to oversee the audit of the Co.'s financial reports

- Determine whether the Co. has a committee of IBMs (Independent Board Members) charged with setting executive remuneration/compensation

- Determine if the Co. has a nominations committee of IBMs that is responsible for recruiting Board Members

- Determine whether the Board has other committees that are responsible for overseeing management's activities in selected areas, such as corp. governance, M&A, legal matters, or risk management.

Investors & shareholders should:MANAGEMENT

- Determine whether the Co. has adopted a code of ethics, & whether the Co's actions indicate a commitment to an appropriate ethical framework

- Determine whether the Co. permits Board Members & management to use Co. assets for personal reasons

- Analyze both the amounts paid to executives for managing the Co's affairs, & the manner in which compensation is provided to determine whether compensation paid to its executives is commensurate with the executives' level of responsibilities & performance, & provides appropriate incentives.

- Inquire into the size, purpose, means of financing & duration of share-repurchase programs & price stabilization efforts.

Investors & shareowners should:SHAREOWNER RIGHTS

- Determine whether the Co. permits shareholders to vote their shares by proxy regardless of whether they are able to attend the meetings in person

- Determine whether shareowners are able to cast confidential votes

- Determine whether shareowners can cast the cumulative number of votes allotted to their shares for one or a limited number of Board norminees

- Determine whether shareowners can approve changes to corp. structures & policies that may alter the relationship btw shareowners & the Co.

- Determine whether & under what circumstances shareowners can nominate individuals for election to the Board

- Determine whether & under what circumstances shareowners can submit proposals for consideration @ the Co's annual general meeting.

- Determine whether the Board & management are required to implement proposals that shareowners approve.

- Examine the Co's ownership structure to determine whether it has different class of common shares that separate the voting rights of those shares form their economic value

- Determine whether the corp. governance code & other legal statutes of the jurisdiction in which the Co. is headquartered permit shareowners to take legal or seek regulatory action to protect & enforce their ownership rights.

- Carefully evaluate the structure of of existing or proposed takeover defenses & analyze how they could affect the value of shares in a normal market environment & in the event of a takeover bid.

IMPORTANT DEFINITIONS

- corporate governance: system of internal controls & procedures by which individual co. are managed. Good corp. governance practices seek to ensure that:

- Board members act in the best interests of shareholders

- related to interest conflict

- the Co. acts in a lawful & ethical manner in their dealings with all stakeholders & their representatives

- all shareholders have the same right to participate in the governance of the Co. & receive fair treatment from the Board & management, & all rights of shareowners & other stakeholders are clearly delineated & communicated.

- the Board & its committees are structured to act independently from management, individuals or entities that have control over management, & other non-shareholders group.

- appropriate controls & procedures are in place covering management's activities in running the day-to-day operations of the Co.

- the Co's operating & financial activities, as well as its governance activities, are consistently reported to shareowners in a fair, accurate, timely, reliable, relevant, complete & verifiable manner

- Independence: a Board member considered as Independent member MUST NOT have a material business or other relationship with some specific individuals/groups

- Board members or Directors: all individuals who sit on the Board, including Executive Board Members, Non-Executive Board Member, Independent Board Members

- Ex-BM: members of executive management

- IBM: individual who meets the "Independence" qualification.

- Non-ex BM: neither Ex-BM nor IBM. represent interests that may conflict with those of other shareowners (such as: union)

- Board: refers to both the Supervisory Board

- Board of Corp. Auditors in countries with a Two-Tier Board structure (such as Japan)

- Board of Directors in countries that use a Unitary Board

Two structures of Board

- Two-Tier Board (Dual Board): has 2 elements: Management Board & Supervisory Board

- Mgnt Board:

- consists exclusively of Ex-mgnt & its charged with running the Co. on a daily basis &

- setting the corp. strategy for the Co.

- do NOT sit on the Co's Supervisory Board

- Sup. Board:

- charged with overseeing & advising the Co's MB

- includes only IBM & Non-Ex BM

- Corp. Auditors System:

- this structure is called Corp. Auditors System & very popular in Japan

- Including:

- Board (<=> Sup. Board)

- Board of Corp. Auditors

- Unitary Board: 2 elements: Boards & Committee system

- Board (<=> Sup. Board)

- may include all: Ex BM, Non-ex BM & IBMs.

- Oversees & advises mgnt & helps set corp. strategy, it could ignore daily activities but can't ignore important matters i.e. mergers, acquisitions, divestitures & sales (spin-off?)

- Committee system

- <=> Unitary Board in Japan (in comparison with Corp. Auditors system)

- use a Board consisting of Ex-BM, IBM & Non-ex BM

- Company:

- firm in which shareonwers have an ownership position

- in which investors are considering an investment

- (hic, so, all positions used "firm" in Corp. finance should be change into "company". the reason is that i'm lazy to type company so i use "firm" for shorter typing)

- Investors: all individuals or institutions who are considering investment opportunities in shares & other securities of the Co.

- Shareowners (shareholders, in my typing /:) ): distinguished from investors by referring only to those individuals, institutions or entities that OWN shares or common or ordinary stocks in the Co.

Wednesday, October 7, 2009

Corp.finance 4: Financial statement analysis (FSA)

Introduction:

In this reading, we use 2 tools to do FSA:

In this reading, we use 2 tools to do FSA:

- Dupont analysis for historical performance: separate ROA, ROE into some parts which could tell more 'bout the performance.

- Pro foma for future forecast

DUPONT ANALYSIS

- Applying for ROA

- = Net income/total assets

- = NI/sales * sales/total assets

- = net profit margin * total asset turnover

- Net profit margin can be analyzed more specific:

- = (Earning before tax - taxes)/sales

- = (EBT-taxes)/EBT * EBT/operating income * operating income/sales

- = (1-taxes/EBT) * EBT/ operating income * operating income/ sales

- = tax burden * interest burden (or: effect of nonoperating item) * operating profit margin

- for ROE:

- = NI/total Equity

- = ROA* total assets/ total equity

- => applied similar analysis

PRO FOMA technique

- Use: forecast future financial statement

- Steps:

Tuesday, October 6, 2009

Corp.finance 3: Working capital Management (1) - cash & Short-term investments

Working capital, including:

Asset:

Short-term liabilities

---

2011.03.22: trong lúc google về mấy mô hình quản lý tài sản ngắn hạn, tìm được file này khá đầy đủ, cụ tỉ, chi tiết. personally mình thấy phần này trong CFA viết ko đầy đủ sâu sắc cho lắm (hay đợi L2, L3 mới sâu sắc thì ko rõ nữa ^^)

Link đây

Asset:

- Cash

- Short-term investments

- Account of Receivable (A/R)

- Account of Payable (A/P)

- Inventories

Short-term liabilities

Measure the efficiency of them in operation activities:

- Ratios

- Current ratio = current asset/current liability = CA/CL (notes: NO AVERAGE!)

- Quick ratio (acid-test ratio) = (cash + short-term marketable investment + Receivables)/CL

- Turnover

- A/R turnover = Credit sales/AVERAGE receivables

- Credit sales: % of sales or if n/a: use industry data

- A/P turnover = Purchases/AVERAGE payables

- Purchase = Ending Inventory - Beginning Inventory + COGS

- Inventory turnover = COGS/AVERAGE inventory

- Days:

- Number of days of Receivables = Accounts Receivable/ AVERAGE day's sales on credit

- = A/R : (credit sales/365)

- Number of days of Payables = A/P / AVERAGE day's purchases

- = A/P : (purchases/365)

- Number of days of Inventory = Inventory/ AVERAGE day's COGS

- = Inventory/ (COGS/365)

- Notes:

- turnovers do NOT EQUAL to 365/number of days; vice versa: Number of days... NOT equal to (1/turnover)*365

- however, when the question does NOT provide enough information => use info. as much as possible

- Inferred definition:

- Operating cycle = No. of days of Receivables + No. of days of Inventory

- NET operating cycle <=> cash conversion cycle = No. of days of Receivables + No. of days of Inventory - No. of days of Payables = Operating cycle - No. of days of Payables

Now, let's talk 'bout managing these 5 items

---

2011.03.22: trong lúc google về mấy mô hình quản lý tài sản ngắn hạn, tìm được file này khá đầy đủ, cụ tỉ, chi tiết. personally mình thấy phần này trong CFA viết ko đầy đủ sâu sắc cho lắm (hay đợi L2, L3 mới sâu sắc thì ko rõ nữa ^^)

Link đây

Monday, October 5, 2009

Corp.finance 2: Cost of capital (Chi phí vốn)

* Definition

* More detailed

1. Cost of debt:

rp = D1/P0

3. Cost of equity

- Cost of capital:

- the rate of return required by capital suppliers: bondholders, stockholders (owners)

- the opportunity cost of funds for the suppliers of capital

- Component of capital: firm has several alternatives for raising capital: bonds, stocks, preferred stock => each source of capital becomes a component of the firm's funding & has a COST => called: component of capital

- Weighted average cost of capital: WACC

- Wd*rd*(1-T) + Wp*rp + We*re

- Wd, Wp, We: the portion of debt, preferred stock, equity, respectively, in total capital (notes: capital, in capital budgeting, NOT includes short-term capital)

- rd, rp, re (or Kd, Kp, Ke): the cost of debt, preferred stock, equity, respectively

- T: tax rate

* More detailed

- Taxes: 'cos debt expenses are deductible => the tax saving is subtracted cost of debt

- Weights

- target capital structure

- current capital structure, @ market value

- average (industry) data

- Marginal cost of capital (MCC) & Investment opportunity schedule (IOS)

- Flotation cost: add to expenses of the year <=> cash out flow; NO add to cost of capital

1. Cost of debt:

- YTM

- Debt-rating approach

- Some features could makes rd higher or lower, depends on the benefit it creates, belongs to whom

rp = D1/P0

3. Cost of equity

- CAPM approach: Ke = E(r) = Rf + beta*(Rm - Rf)

- DDM approach: Ke = D1/P0 + g

- g = growth rate = (1 - D/EPS)*ROE = b*ROE

- b = company's earning retention rate = 1 - D/EPS

- Bond yield plus risk premium approach: E(r) = bond yield + risk premium (notes: bond yield NO deducting tax)

- Adjust for country risk

- country equity premium = sovereign yield spread * (annualized standard deviation of equity index/ annualized standard deviation of the sovereign bond market in terms of the developed market currency)

- Or, in short: Rc = delta Rf * SDe/SDd

- affection to E(r) in CAPM: E(r) = Rf + beta * [(Rm - Rf) + Rc]

- Estimating beta?

- beta equity (or beta levered) ### beta asset (or beta unlevered)

- beta asset = beta equity / [1+ ((1-t)*D/E)]

- beta equity = beta asset* [1 + (1-t)*D/E]

- Estimating a beta using the pure-play method

- select the comparable: determine comparable company or companies operating in similar business risk

- estimate those comparable companies' equity beta

- unlever the equity beta at (2) => beta asset

- lever the beta asset at (3) (for the financial risk of the considering company/project) => equity beta of the considering company/project

Sunday, October 4, 2009

Corp.finance 1: Capital budgeting (hoạch định ngân sách vốn đầu tư)

* Role, meanings

- liên quan tới cơ cấu tài sản & cơ cấu vốn <=> ảnh hưởng đến toàn bộ hoạt động của DN

* Steps of capital budgeting:

- liên quan tới cơ cấu tài sản & cơ cấu vốn <=> ảnh hưởng đến toàn bộ hoạt động của DN

* Steps of capital budgeting:

- generating idea

- analyzing individual proposal

- planning the capital budgeting

- monitoring & post-auditing

Monday, September 21, 2009

Kinh tế vi mô (3): Các hành vi trong thị trường (market in action)

Như đã nói trong bài trước, có 6 yếu tố làm cản trở sự hiệu quả & công bằng trong phân phối nguồn lực. Trong bài này, chúng ta sẽ nghiên cứu 2 trong số 6 yếu tố đó, gồm có:

Okie, let's start!

- Price ceiling & price floor (giá trần & giá sàn)

- Taxes & subsidies (thuế & trợ cấp & nhân tiện, nghiên cứu thêm cả quota)

Okie, let's start!

Kinh tế vi mô (4): Organizating Production (Tổ chức sản xuất)

Sau khi đã "dạo quanh phố phường, dạo qua thị trường", giờ chúng ta sẽ view kỹ hơn vào từng firm. Bài này trả lời các câu hỏi:

- Mục tiêu của 1 cty là gì?

- Để đạt đc mục tiêu đó thì cty fải làm gì?

- Những việc làm ở (2) lại gặp fải các constraints (trở ngại), cụ tỉ là: technological constraint, information constraint, & market constraint => đối fó với n~ constraint này ra sao?

- Cuối cùng, tại sao cty sản xuất cái lọ & mua cái chai - sx bởi n~ cty khác trên thị trường, thay vì sx cái chai & mua cái lọ?

Saturday, August 29, 2009

Kinh tế vi mô (2): Hiệu quả và công bằng (Efficiency & Equity)

Bài này bàn về tính Hiệu quả và Công bằng (Efficiency & Equity) khi phân bổ các nguồn lực - vốn khan hiếm, trong XH.

Như ta đã biết (hoặc nếu chưa biết thì bây h biết ;) ), 1 trong 10 nguyên lý kinh tế học đó là: nguồn lực thì có hạn nhưng nhu cầu của con ng` là vô hạn => luôn fải đối mặt với sự khan hiếm nguồn lực & do đó, fải đánh đổi. Câu hỏi là: con người đánh đổi ntn? Về mặt nguyên tắc, 1 người sẽ lựa chọn sao cho tối đa hóa lợi ích của họ, nói cách khác, sử dụng thời gian + tiền bạc của họ sao cho phần nguồn lực khan hiếm họ nhận đc là lớn nhất.

Đối với xã hội, lợi ích xã hội đc tạo ra khi thị trường kết hợp các quyết định của mỗi cá nhân lại với nhau.

Trước khi bàn về tính hiệu quả và công bằng, ta sẽ đề cập đến n~ phương pháp được sử dụng để fân bổ các nguồn lực. Cụ thể, có 8 pp như sau:

Như ta đã biết (hoặc nếu chưa biết thì bây h biết ;) ), 1 trong 10 nguyên lý kinh tế học đó là: nguồn lực thì có hạn nhưng nhu cầu của con ng` là vô hạn => luôn fải đối mặt với sự khan hiếm nguồn lực & do đó, fải đánh đổi. Câu hỏi là: con người đánh đổi ntn? Về mặt nguyên tắc, 1 người sẽ lựa chọn sao cho tối đa hóa lợi ích của họ, nói cách khác, sử dụng thời gian + tiền bạc của họ sao cho phần nguồn lực khan hiếm họ nhận đc là lớn nhất.

Đối với xã hội, lợi ích xã hội đc tạo ra khi thị trường kết hợp các quyết định của mỗi cá nhân lại với nhau.

Trước khi bàn về tính hiệu quả và công bằng, ta sẽ đề cập đến n~ phương pháp được sử dụng để fân bổ các nguồn lực. Cụ thể, có 8 pp như sau:

Thursday, August 27, 2009

Kinh tế vi mô (1): Độ nhạy cảm (elasticity)

Chúng ta sẽ nghiên cứu lần lượt độ nhạy cảm của Cầu & Cung theo giá.

ĐỘ NHẠY CẢM CỦA CẦU THEO GIÁ

Độ nhạy cảm của cầu theo giá (Price Elasticity of Demand): cho biết khi giá tăng/giảm 1% thì lượng cầu giảm/tăng tương ứng là bao nhiêu %. Công thức tính:

Chú ý trong công thức trên:

ĐỘ NHẠY CẢM CỦA CẦU THEO GIÁ

Độ nhạy cảm của cầu theo giá (Price Elasticity of Demand): cho biết khi giá tăng/giảm 1% thì lượng cầu giảm/tăng tương ứng là bao nhiêu %. Công thức tính:

PE = %Qd_change/%P_changes= [|Qd2-Qd1|/((Qd1+Qd2)/2)]/[|P2-P1|/((P2+P1)/2)]

Chú ý trong công thức trên:

- P, Q lấy giá trị trung bình ((P2+P1)/2 và (Qd1+Qd2)/2) => thể hiện mức nhạy cảm của lượng cầu khi P tăng từ P1 tới P2 hoặc giảm từ P2 về P1 là NHƯ NHAU

- Vì đối với hàm cầu: P tăng thì Q luôn giảm & ngược lại => dấu ko quan trọng

- Vì là %/% => kquả là ko có đơn vị => có thể so sánh giữa các loại hàng hóa khác nhau.

Subscribe to:

Posts (Atom)