ko quên add luôn bài về on-the-run vs off-the-run fixed income nói chung & TIPS nói riêng từ blog bác Giang

source:http://krugman.blogs.nytimes.com/2009/11/09/tips-and-inflation-expectations/

[hahah, fải để source to oành vậy vì mìh sợ violate standard of professional, hnhư là I.C thì fải, misrepresentation :)) ]

November 9, 2009, 8:58 am

TIPS and inflation expectations

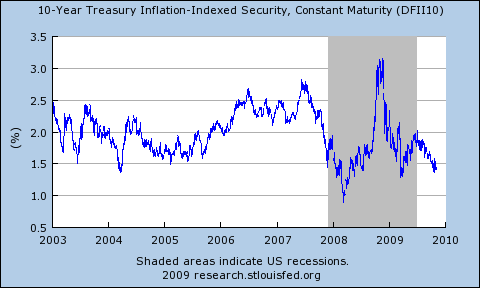

You can see what I mean in the chart above. The yield on TIPS shot up after Lehman fell; ordinary bond yields plunged over the same period. Was this a collapse in expected inflation? Not really, or at any rate not mostly: TIPS are less liquid than regular 10-year bonds, so in the rush for liquidity they became very underpriced for a while. Correspondingly, as markets calmed down there was a fall in TIPS yields and a rise in ordinary bond yields; this probably didn’t have much to do with changing inflation expectations.

So when you read something like this:

Market inflation expectations can be calculated by comparing the difference in yields on a 10-year Treasury and a 10-year Tip. In the US, that gauge has reached the highest level in 15 months. A comparison of similar UK bonds shows expectations are at an 11-month high.you have to take it with large helpings of salt. [i like this :)) ]

This rise has led to talk of a return of “bond vigilantes”, investors who in the past have pushed up long-term bond yields on fears of inflation and forced central bankers to tighten policies.

Oh, and this particular story did something I’ve noticed more and more in financial reporting: when reporters are assigned to write a story about how bond markets are afraid of debt/deficits/inflation, they have a strange and telling habit of telling readers a lot of scare stories about how markets are nervous, along with something about how interest rates or spreads are at their highest level in x weeks or y months — but strangely fail ever to mention what the spreads or rates actually are. Thus I’ve read scary-sounding articles about Japanese debt that somehow never mention that Japan is currently able to borrow long-term at less than 1.5%.

And in this case you’d never know from the story what the 10-year U.S. inflation rate implied by the TIPS spread is. The answer, as of Friday, was 1.98 percent. But that number sort of wouldn’t match the whole thing about bond vigilantes, I guess, so it was omitted.

No comments:

Post a Comment